The AI Spend Simply Doesn't Add Up: How Uber, Klarna, and Duolingo Became the Face of a $700 Billion Accountability Crisis

There is a moment in every financial cycle when the question everyone was too polite to ask gets asked anyway, and for the AI industry, that moment appears to have arrived. And this isn’t an announcement by a short-seller or a sceptical analyst but by the COO of Uber, which ironically is one of the most AI-committed consumer technology companies in the world.

Speaking on the Rapid Response podcast, Andrew Macdonald, President and Chief Operating Officer of Uber, described the conversation his company was having with its own engineering leadership. "It's amazing, and I think it's this massive transformation of society," he said, "but then you sometimes go and you talk to your senior engineering leaders, and you're saying, 'okay, how many projects that were on the cutting room floor got moved above the line because of the productivity gains, because 25% of our code commits were via Claude Code last quarter?' That link is not there yet."

While measured and said in an optimistic tone, the substance just doesn’t match up. The substance was not. Uber had already burned through its entire 2026 AI budget by March.

Macdonald described the moment the company's CTO, Praveen Neppalli Naga, admitted as much in an interview and went viral: "Everyone was like, you know, head-exploding moment. We're going to have to start talking about token consumption and the associated costs relative to headcount, and, like, making trade-offs on that as an engineering organisation. And so if you're not actually able to draw a direct line to how many useful features and functionality you're shipping to your users, that trade becomes harder to justify."

On Uber's first-quarter earnings call in May, CEO Dara Khosrowshahi confirmed the company was slowing hiring as a direct consequence of its AI investment. He cast it as a bet on productivity still to come. "If every person at this company can increase their throughput by 20%, 30%, 50%, 100%," Khosrowshahi said, "then I think metering headcount growth and leaning in on AI investment is going to be well worth it." He also noted that roughly 10% of the company's code changes were now produced by autonomous agents. It was a statement of faith rather than of demonstrated return: the spending is real, the hiring restraint is real, and the productivity gain that would justify both has not yet materialised at a measurable scale.

Duolingo's experience ran a similar arc. In April 2025, CEO Luis von Ahn announced that the company would become "AI-first" and formally evaluate employees' AI use during performance reviews. The backlash was swift enough that von Ahn was walking back elements of the announcement within a week.

By April 2026, he had removed AI use as a performance metric entirely, explaining the reversal on the Silicon Valley Girl podcast. "At the end, we backtracked," he said. "The most important thing in your performance is that you are doing whatever your job is as well as possible. A lot of times, AI can help you with that, but if it can't, I'm not going to force you to do that." He acknowledged the company had been "trying to push something that in some cases did not fit." Employees had asked him directly whether the metric existed simply to prove AI use for its own sake. He concluded that it did. Duolingo's share price is now 81% off its May 2025 peak.

Klarna Wrote the Cautionary Case Study in Real Time

The most instructive recent case, and one that predates Uber's public reckoning, belongs to Klarna. In 2023, CEO Sebastian Siemiatkowski partnered with OpenAI and declared that Klarna would become the technology's "favourite guinea pig." The company froze non-engineer hiring, cut its workforce from 3,800 to 2,000 through attrition, and deployed an AI chatbot it claimed was handling two-thirds of customer service conversations, the equivalent of 700 human agents, within its first month. The numbers were real, but the conclusion drawn from them was not.

By mid-2025, with Klarna preparing for its IPO, Siemiatkowski told Bloomberg something different. "From a brand perspective, a company perspective, I just think it's so critical that you are clear to your customer that there will always be a human if you want," he said. The company began recruiting human agents again, targeting students, remote workers, and professionals, describing the reversal as an evolution.

Separately, Siemiatkowski acknowledged the underlying problem more directly: "We focused too much on efficiency and cost. The result was lower quality, and that's not sustainable." Klarna had pitched itself to public market investors partly on the strength of its AI-first customer service model.

Within months of going public, its CEO confirmed that the model had produced inferior outcomes and that the company was rehiring humans. Starbucks, facing comparable operational errors from its AI model that it could not contain at scale, reached the same conclusion and cancelled the deployment altogether.

The Enterprise Failure Rate Is Not a Rounding Error

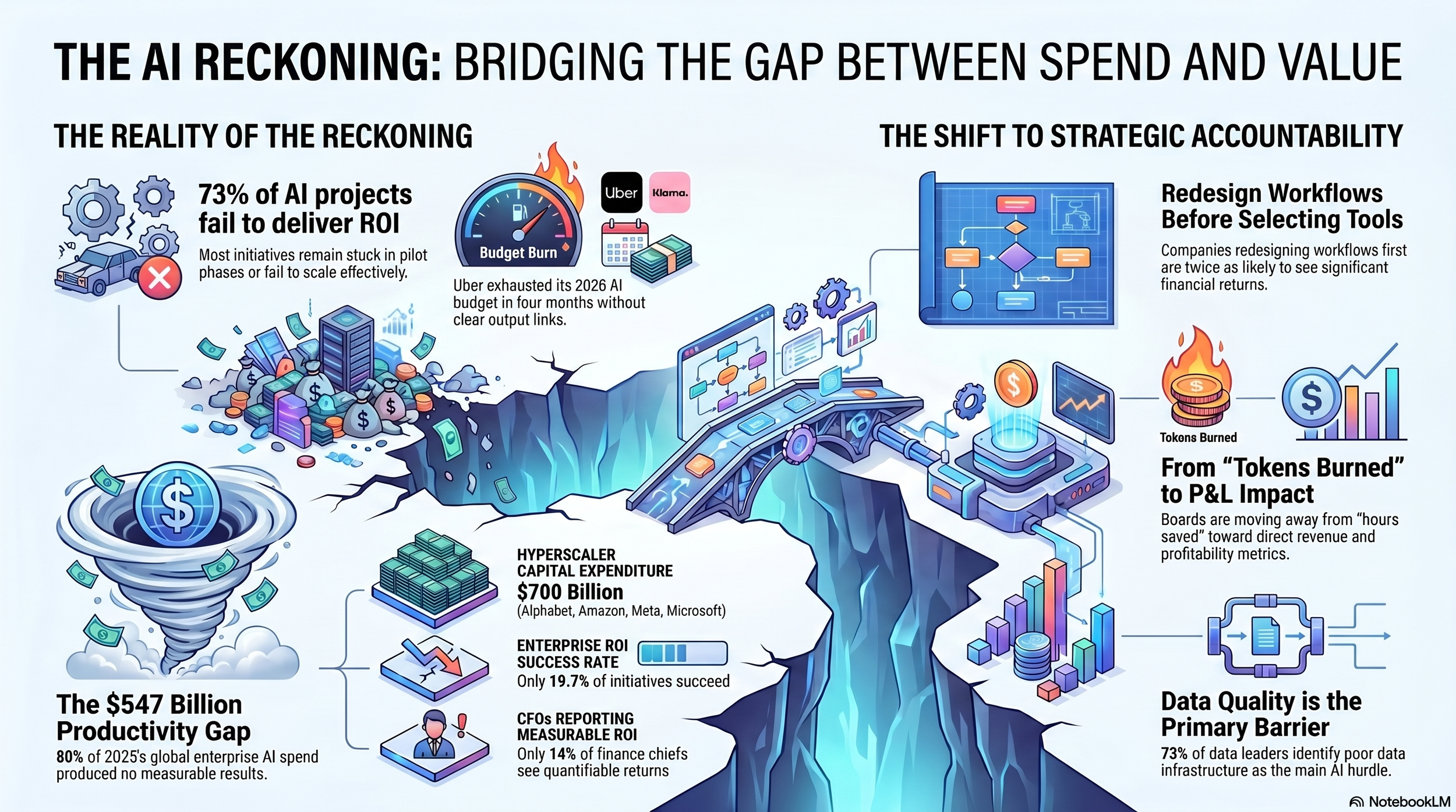

What Uber, Duolingo, Klarna, and Starbucks are experiencing individually, the data describes collectively. Orgvue's May 2026 survey of more than 1,000 C-suite and senior decision-makers found that 78% of organisations have had AI projects either fail outright (35%) or remain stuck in pilot (43%), despite record investment. The survey is in its third consecutive year of tracking these outcomes. The picture has not improved. Thirty-two percent of respondents said they still do not understand how to make AI work; 49% have committed to upskilling programmes because they lack the talent to deploy it successfully.

The McKinsey Global AI Survey 2026 put the ROI failure rate at 73%, a figure that has remained stubbornly consistent despite improvements in model capabilities. Gartner's survey of 782 infrastructure and operations leaders found only 28% of AI use cases fully met ROI expectations, with 20% failing outright.

BCG's September 2025 research found 60% of companies generating no material value despite continued spending. A separate Gartner forecast predicts that 60% of AI projects lacking AI-ready data infrastructure will be abandoned through 2026, which covers a significant proportion of current deployments, given that a Capital One and Forrester study found 73% of enterprise data leaders identified data quality as their primary AI barrier.

RAND's analysis of more than 2,400 enterprise AI initiatives found that 80.3% failed to deliver intended business value, broken down as follows: 33.8% abandoned before reaching production, 26.5% reached deployment but failed to scale, and 20% delivered some value but not enough to justify continued investment.

Only 19.7% succeeded by any reasonable measure. The Futurum Group's first-half 2026 survey of 830 IT decision-makers captured what may be the most consequential shift: productivity gains have collapsed as the leading AI ROI metric, falling from 23.8% to 18%, while direct financial impact, combining revenue growth and profitability, nearly doubled as the standard boards and CFOs now demand. Keith Kirkpatrick, Vice President and Research Director at Futurum, was blunt about the implications: "Sales teams leading with 'save 4 hours per week' are entering a losing conversation."

Writer's 2026 survey of 2,400 global enterprise leaders produced a number that sits at the centre of the problem: 97% of executives report personally benefiting from AI, but only 29% see significant organisational ROI. Morgan Stanley, looking across the S&P 500, found that only 21% of companies could cite a measurable AI benefit. Only 14% of CFOs, according to CFO.com research, currently report measurable ROI from their AI spending. That means 86% of finance chiefs are funding AI programmes they cannot quantify.

The Infrastructure Spend Has Decoupled from Any Revenue Thesis That Currently Holds

While enterprise buyers pull back from pilots that are not producing, the infrastructure buildout above them is accelerating to a degree that makes the demand-side uncertainty considerably more dangerous. The four largest hyperscalers, Alphabet, Amazon, Meta, and Microsoft, have committed to spending approximately $700 billion on capital expenditure in 2026, nearly double the $388 billion they spent in 2025. Amazon is projecting $200 billion alone.

Microsoft has set its calendar-year figure at $190 billion, of which CFO Amy Hood attributed $25 billion to rising memory chip and component costs. Epoch AI's tracking shows combined hyperscaler capex has grown at an average of 72% per year since the second quarter of 2023, having quadrupled since the release of GPT-4. Amazon's free cash flow has declined by 95% on a trailing 12-month basis to $1.2 billion.

The revenue side of that equation is a fraction of the commitment. A Praetorian Capital analysis by fund analyst Lauren Cousyn, published last October, attempted the arithmetic the industry had consistently avoided. It found that the AI infrastructure sector spends over $30 billion a month while receiving roughly $1 billion a month in revenue.

Cousyn's updated breakeven calculation, after consulting more than two dozen senior datacenter professionals, concluded the industry needs between $320 billion and $480 billion in annual revenue just to break even on 2025's capex, against current revenues of $15 to $20 billion. The most consistent finding from those conversations: "no one understands how the financial math is supposed to work" -- including the people running the infrastructure. The paper noted that, contrary to Cousyn's initial modelling, AI datacenters depreciate on a three-to-five-year cycle rather than ten years, which makes the capital destruction on any failed deployment considerably more severe.

Gartner's 2026 trend report puts total AI-driven spending across hardware, software, and applications at $2.52 trillion this year, a 44% year-over-year increase. Cumulative investment is now approaching $3 to $4 trillion by the end of the decade on current trajectories. The gap between what is being committed at the infrastructure level and what is being verified as value at the enterprise level is not a temporary lag. It is the central financial tension of the current AI cycle, and no major participant has yet provided a satisfactory account of how it will be resolved.

Token Consumption Was Never a Proxy for Value Creation

The Uber situation is instructive not just as a data point but as a structural diagnosis. Macdonald identified something precise: the decoupling of AI consumption from measurable output is not a technical failure. Uber's code commit figures, a quarter of all commits running through Claude Code, are by most measures an impressive deployment metric. The problem is that impressive deployment metrics are not output metrics. Tokens burned, compute cycles consumed, and API calls made are inputs. The engineering discipline required to translate model access into shipped, functioning product is distinct from the discipline of procuring model access. Many organisations conflated the two.

KPMG research captures the speed of the shift in what investors now require: pressure for demonstrated AI ROI jumped from 68% of organisations in the fourth quarter of 2024 to 90% in the first quarter of 2025, in a single quarter. A Teneo survey found 53% of investors expect AI projects to pay off within six months, while only 16% of CEOs believe that is realistic. The 71% of CIOs who expect budget cuts if they miss mid-2026 targets are now operating inside that tension in real time. The era of productivity metrics as AI ROI is over.

ClarityArc's May 2026 research, drawing on board-level data, was direct: the organisations keeping their AI budgets intact are those that built measurement infrastructure before deployment and can now point to specific P&L lines. Those facing cuts are the ones who approved spending on projected efficiency gains and cannot connect the results to a financial outcome their CFO recognises as evidence of return.

Folio3's April 2026 analysis offered one of the more arresting characterisations of 2025's record. Enterprises poured $684 billion into AI last year. By year-end, more than $547 billion of that investment had produced no measurable results. Not low returns. None. The caveat worth applying is that measuring the counterfactual is genuinely difficult, and some of that spend may have purchased infrastructure or organisational capability that will compound later. But measurable evidence at the P&L level in the current data is largely absent.

What a $700 Billion Year Needs to Produce, and What Happens If It Doesn't

The investment has not been wasted in totality. There are genuine enterprise deployments, particularly in legal document review, code assistance, and structured customer service routing, where productivity gains are real and measurable. The 5% of organisations BCG found to be creating substantial AI value at scale are doing so under conditions the majority have not replicated: clean data environments, redesigned processes, human oversight built into workflows, and measurement structures tied to business outcomes rather than activity metrics. McKinsey's 2025 research found that companies which redesigned workflows before selecting AI tools were twice as likely to report significant financial returns. Most companies did the opposite.

The Praetorian Capital analysis drew a direct comparison to the transcontinental railroad buildout, where the infrastructure was strategically necessary, and the individual economics were ruinous, producing multiple financial panics when funding stalled. The fibre optic buildout of 2000 followed the same pattern: real infrastructure, genuine capability, and a capital structure that collapsed when the gap between investment and revenue became undeniable.

The analysis carefully noted that collapse is not imminent, that power contracts lock in multi-year commitments, that long-lead hardware orders have been placed, and that the buildout will continue in the medium term regardless of whether revenue follows. What it raised was a question about the broader economy, which it estimated was absorbing the equivalent of more than 2% of US GDP in AI capital expenditure, and what happens when the gap between investment and demonstrable return becomes impossible to defer.

Macdonald's phrasing on the Rapid Response podcast was "not there yet" rather than "not there." The optimism embedded in that framing is not implausible. AI capabilities have improved faster than most practitioners predicted, and there are real enterprise use cases where the case is closed. But the direction of travel he was describing was that Uber is spending more, shipping less in proportion, and slowing hiring to sustain the spend, at the same moment that 78% of organisations globally report their AI projects have failed or stalled, that $547 billion of last year's enterprise AI investment produced nothing measurable, and that the hyperscalers are committing another $700 billion this year on the same bet.

The industry's response to this moment will matter. The optimistic reading is that what is happening is a necessary and healthy tightening of deployment standards: better measurement, more disciplined use-case selection, workflow redesign before procurement. The less comfortable reading is that a significant portion of the capital already deployed and a considerably larger portion being committed for 2026 is riding on a revenue and productivity thesis that the current evidence does not support.

Both readings can be partly true; what Uber, Duolingo, Klarna, and Starbucks collectively demonstrate is that the thesis requires proof, that proof requires measurement, and that measurement has been the industry's most consistent failure. The open question is how long the capital markets are willing to carry uncertainty before they demand a definitive answer.