Luxury brands in the Gulf are losing control of how consumers discover them, says report by Snap and the Business of Fashion

At Shop Talk Luxe in Abu Dhabi, Snap Inc. and the Business of Fashion unveiled a new report on fashion and beauty consumption in the Gulf. Like many industry launches, it arrived wrapped in familiar claims about youth, technology and opportunity. What made it worth paying attention to was not the optimism, but what it revealed about how the relationship between brands and consumers in the GCC is quietly changing.

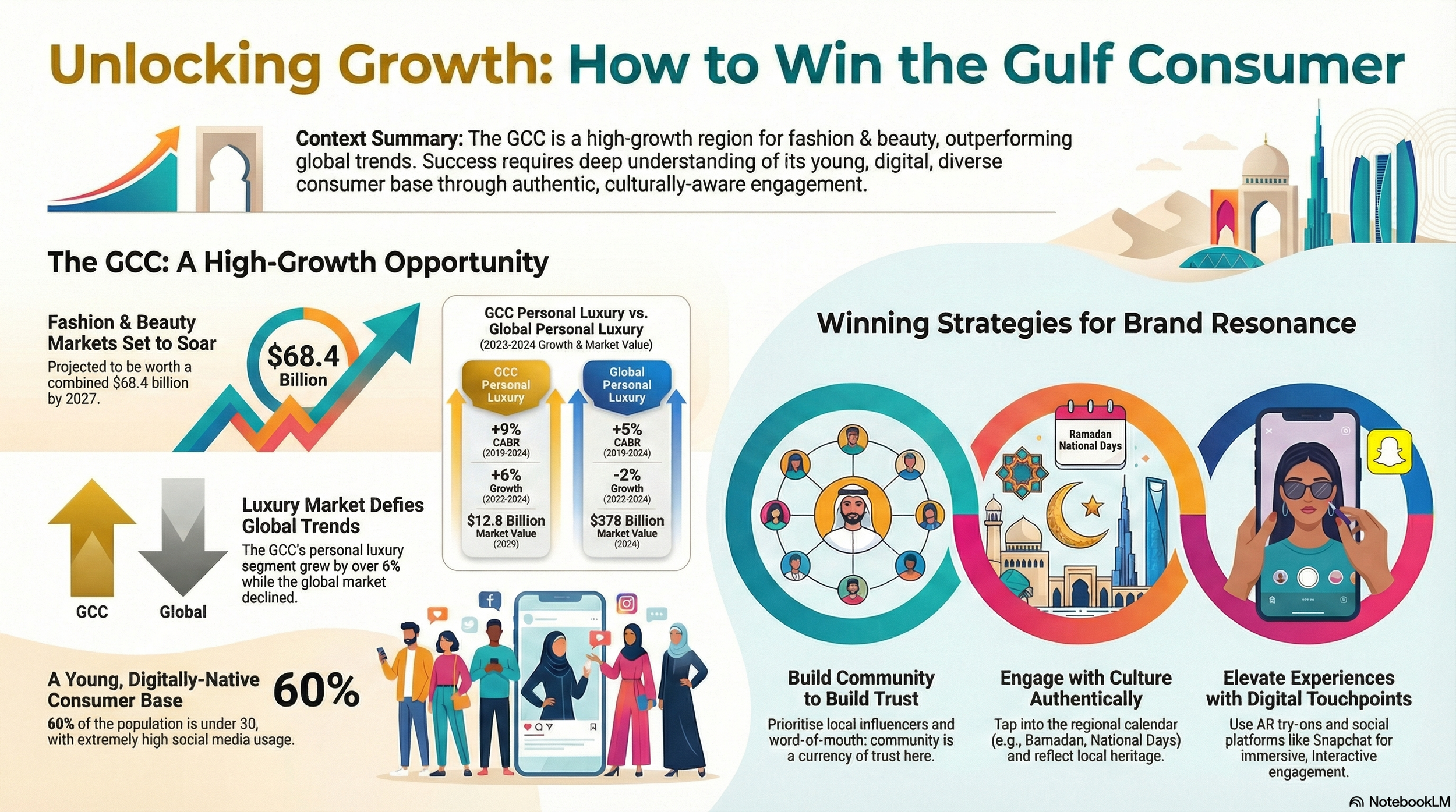

The report, Building Brand Resonance With Gulf Consumers, is positioned as a guide for luxury executives navigating one of the industry’s fastest-growing regions. In practice, it reads more like a diagnosis of why established playbooks no longer travel cleanly into the Gulf, even as spending power rises.

A young market with its own logic

Much of the demographic context is already well known. Around 60% of the GCC population is under 30. In Saudi Arabia, women’s participation in the workforce rose sharply between 2018 and 2020, reshaping household incomes and decision-making. What the report usefully underscores is how these shifts have altered the social mechanics of consumption.

Luxury purchases in the Gulf are rarely private acts. They are discussed within families, shaped by peer opinion and often validated away from public feeds. According to the report, 77% of Snapchat users in the GCC share or recommend products to friends and family. That behaviour helps explain why traditional broadcast-style marketing often underperforms, even when brand awareness is high.

“The GCC is at the forefront of digital innovation,” said Hussein Freijeh, Vice President for Snap Inc. MENA & APAC, at the launch event. “As consumer expectations continue to evolve, brands will need to find ways to reach and engage the next generation of consumers.”

Stripped of event language, the point is straightforward. Brands in the Gulf increasingly reach consumers through intermediaries they do not control. Discovery, discussion and recommendation happen inside messaging apps, creator networks and private social spaces. Snapchat has become one of those spaces, not because it replaces retail, but because it shapes intent before retail begins.

For brands, that shifts where influence sits. Marketing is less about projecting aspiration and more about fitting into existing social exchanges.

Augmented reality as a practical tool

Globally, augmented reality is still often treated as experimental. In the Gulf, it has found a clearer use case. The report notes that 70% of Snapchat users worldwide engage with AR features, with particularly strong uptake in the GCC. Virtual try-ons for fashion and beauty are highlighted not as spectacle, but as tools that reflect local conditions. Climate, mall culture, privacy norms and time constraints all shape how people shop in the region.

“Snapchatters in MENA are turning to Snapchat to shop, discover and learn about fashion and beauty products,” Freijeh said, pointing to AR-powered try-ons and creator collaborations.

The significance is not technological novelty. It is convenience. AR allows consumers to explore products with low commitment and arrive at physical retail better informed.

Culture cannot be added at the end

One of the report’s more grounded observations is that cultural relevance in the GCC cannot be applied late in the process. Activations around Ramadan, National Day or local heritage resonate when they reflect lived experience rather than imported templates.

This is where many global brands struggle. They localise language and visuals but miss the behavioural context. Platforms embedded in daily communication patterns see those mismatches quickly, which in turn gives them disproportionate influence over what feels authentic and what does not.

For brands, that means technology partners increasingly shape cultural understanding, not just distribution.

What the report is really telling executives

The Snap and Business of Fashion partnership reflects a wider shift playing out across global consumer markets. Growth regions are asserting their own rhythms and expectations, and a single global luxury narrative no longer scales without friction.

In that environment, the path between brand and consumer has narrowed and become more mediated. Access depends less on visibility and more on whether a brand fits naturally into the systems where people already talk, share and decide.

Luxury in the Gulf continues to expand. What is changing is not demand, but the route to it. The brands that adapt will be those that understand this shift early and treat technology not as an add-on, but as part of how legitimacy is earned in the market.