Saudi Arabia and UAE Rank in Global Top 10 for AI-Enabled Finance, as New Index Redefines What It Means to Lead in AI

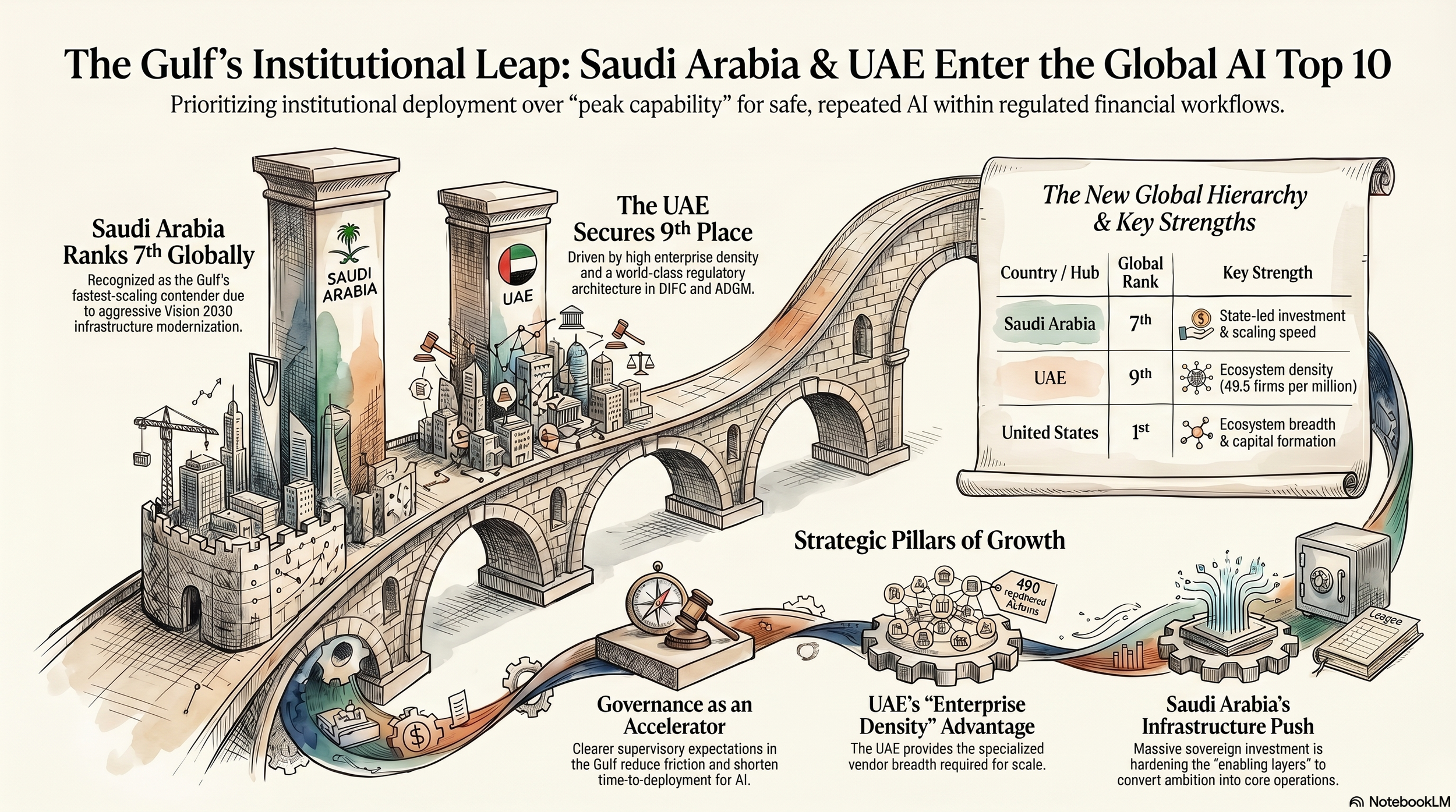

Saudi Arabia and the UAE have placed 7th and 9th, respectively, in the fifth edition of the Global AI Competitiveness Index, the first in the series dedicated entirely to financial services, according to a report published by the AI Index Consortium with technical support from Deep Knowledge Group and the Financial Services Development Council serving as Observer. The index ranks 20 countries and 15 city-level finance hubs on AI-for-Finance capability and maturity, and its central finding reorders the conventional hierarchy of AI leadership: the countries winning the AI race in financial services are not those building the most powerful models. They are the ones that can deploy those models safely, repeatedly, and at an institutional scale inside regulated workflows.

That distinction is the single thread running through the entire report, and it has direct implications for both Gulf nations as they continue to scale their AI ambitions.

A Different Kind of Race

The country index is led by the United States at 98.84 and China at 83.41, followed by the United Kingdom at 78.26 and Switzerland at 73.09, with Singapore rounding out the top five at 69.12, according to the index's pillar-based scoring framework. The US position will surprise no one. China's will. Most Western-authored AI assessments measure using metrics in which the US and Europe hold structural advantages: research output, venture capital formation, and foundational model development. This index applies a different filter, and on it, China performs exceptionally. Of the 20 countries ranked, China outperformed every other nation in financial-sector AI maturity, earning a score of 90 for its adoption of AI across banking, insurance, fintech, and investment management. The report describes China as the strongest among the top-ranked countries at translating AI capacity into production-grade deployment in financial services — what it calls the last mile from capability to operational systems.

What separates the leaders from the middle of the table is not a single outstanding strength. According to the report, the leaders are defined by multi-pillar performance that supports production-grade AI in finance, including deployment readiness, institutional capacity, and ecosystem breadth. A country with excellent AI research output but weak supervisory infrastructure will underperform in this index. So will one with strong capital markets but fragile data systems. The index is a test of systemic depth, not peak capability.

The Gulf's Position and What It Reveals

The report describes Saudi Arabia as the Gulf's fastest-growing contender in AI-enabled finance, attributing its 7th-place ranking to state-led investments and a strategic focus on modernising financial infrastructure, which has characterised the Kingdom's approach under Vision 2030. The UAE's 9th place reflects a different but complementary strength. According to the index, the country ranks 9th in the world for AI enterprise density at 49.5 AI firms per million people, and holds 19th globally in total AI company count, with 490 registered firms, including two unicorns. That density matters in the context of financial services AI because ecosystem breadth — the availability of specialised vendors, compliance technology providers, and AI-native infrastructure players — is one of the key variables determining how quickly regulated institutions can move from pilot to production.

Dmitry Kaminskiy, General Partner of Deep Knowledge Group, noted in the report's release that the UAE's unique position in the index highlights its ability not just to innovate but to efficiently deploy AI systems that meet the rigorous demands of regulated financial markets.

The UAE has been building its position through several converging mechanisms: regulatory architecture at the DIFC and ADGM, sovereign capital directed at AI infrastructure, including the Stargate project backed by OpenAI and NVIDIA, and governance positioning that gives it credibility with international counterparts. The UAE's AI Strategy 2031 targets a contribution of AED335 billion to the country's GDP through AI-driven innovation, alongside a 50% reduction in government operational costs through AI adoption. That ambition is now backed by measurable structural indicators, which is precisely what this index captures. The DIFC is also set to host the Global Privacy Assembly in the fourth quarter of 2026, the first time the event has come to the Gulf, a recognition of the UAE's growing standing within global data protection and AI governance circles, according to analysis published by Crowell and Moring.

At the city level, Riyadh appears in the mid-table hub cluster alongside Toronto, Singapore, Tokyo, and Chicago. The report characterises mid-table hubs as typically showing strengths in one or two dimensions but lacking complete end-to-end breadth, often constrained by thinner ecosystem density, fewer scalable deployment pathways into regulated institutions, or weaker global market connectivity. The report is direct about what closing that gap requires: stronger capital formation and listing pathways, expanded adoption mechanisms for production-grade technologies across regulated institutions, and sufficient ecosystem breadth to convert AI capabilities into repeatable, auditable deployments rather than isolated pilots.

The Governance Advantage

The report's most consequential argument is that regulatory clarity has become an accelerator rather than a constraint on AI deployment. The conventional framing positions governance and speed as being in tension. The index's findings reverse that assumption. According to the report, clearer supervisory expectations reduce friction and shorten time-to-deployment. When financial institutions know precisely what standards their AI systems must meet — what auditability means in practice, what operational resilience looks like from a regulator's perspective — they can build toward those standards rather than stalling in uncertainty.

Model governance and assurance are now central to competitive positioning, with monitoring, auditability, and operational resilience becoming baseline expectations across the index's top-ranked markets. Generative AI is entering this territory too. Competitive advantage now depends less on who runs the most ambitious experiments and more on who can demonstrate controls, traceability, and resilience when those experiments reach institutional-scale production. Dr Patrick Glauner, Professor of AI at Deggendorf Institute of Technology and a co-author of the report, described the finding directly: in finance, competitive advantage comes from trustworthy AI models that are explainable, auditable, and robust under real-world constraints.

Risk and compliance are identified in the report as the decisive use cases in AI-enabled finance, with the most scalable value in risk modelling, surveillance, and compliance automation. These are unglamorous applications compared to generative AI assistants or autonomous trading systems, but they illustrate where AI delivers consistent, measurable, and auditable performance within institutions that cannot afford failure. The report identifies them as competitive signals, not incremental improvements, because they determine whether a jurisdiction's AI activity compounds into a structural advantage or remains perpetually at the pilot stage.

The Flywheel Dynamic

The city-hub rankings expose the extent to which AI-for-finance activity is geographically concentrated and explain why. New York scores 99, London 81, and Hong Kong 76. San Francisco at 70 and Shanghai at 67 follow, each reflecting what the report describes as the interaction between AI capability and financial-market pull. The index introduces the concept of a finance-tech flywheel to explain the self-reinforcing nature of these rankings: institutional adoption at scale pulls in vendors and talent, deepening the ecosystem and attracting more institutional demand. Market infrastructure, particularly listing ecosystems and capital formation pathways, converts that momentum into durable growth. The cities at the top have been running this flywheel for long enough that it is difficult to disrupt from the outside.

For the Gulf, the flywheel dynamic defines the task ahead. The capital is present. The regulatory intent is established. The sovereign investment in infrastructure is among the most aggressive globally. The report notes that jurisdictions which harden enabling layers can climb fastest as AI adoption accelerates. The bottleneck is institutionalisation: whether AI adoption inside Gulf financial institutions is reaching into core operations, or remaining concentrated in innovation units and showcase deployments. The gap between 7th place and the top five, between Riyadh as a mid-table hub and New York or London, is not a gap in ambition. It is a depth gap, and it is closeable.

The report draws a direct parallel between investment in AI talent and infrastructure and the historical strategic value placed on oil and rare-earth metals. Countries that invest now in technical capacity and governance credibility will be better positioned across the next decade. For a region that understands, better than most, how resource advantage translates into lasting economic architecture, that framing is not rhetorical. It is a roadmap.