Building AI and Deploying It Are Not the Same Thing — China Just Proved It

The country that has built the most powerful AI models is not the country that has done the most with them inside its financial system. That gap is the most consequential finding in the fifth edition of the Global AI Competitiveness Index, published by the AI Index Consortium with technical support from Deep Knowledge Group, and its implications extend well beyond the rankings themselves.

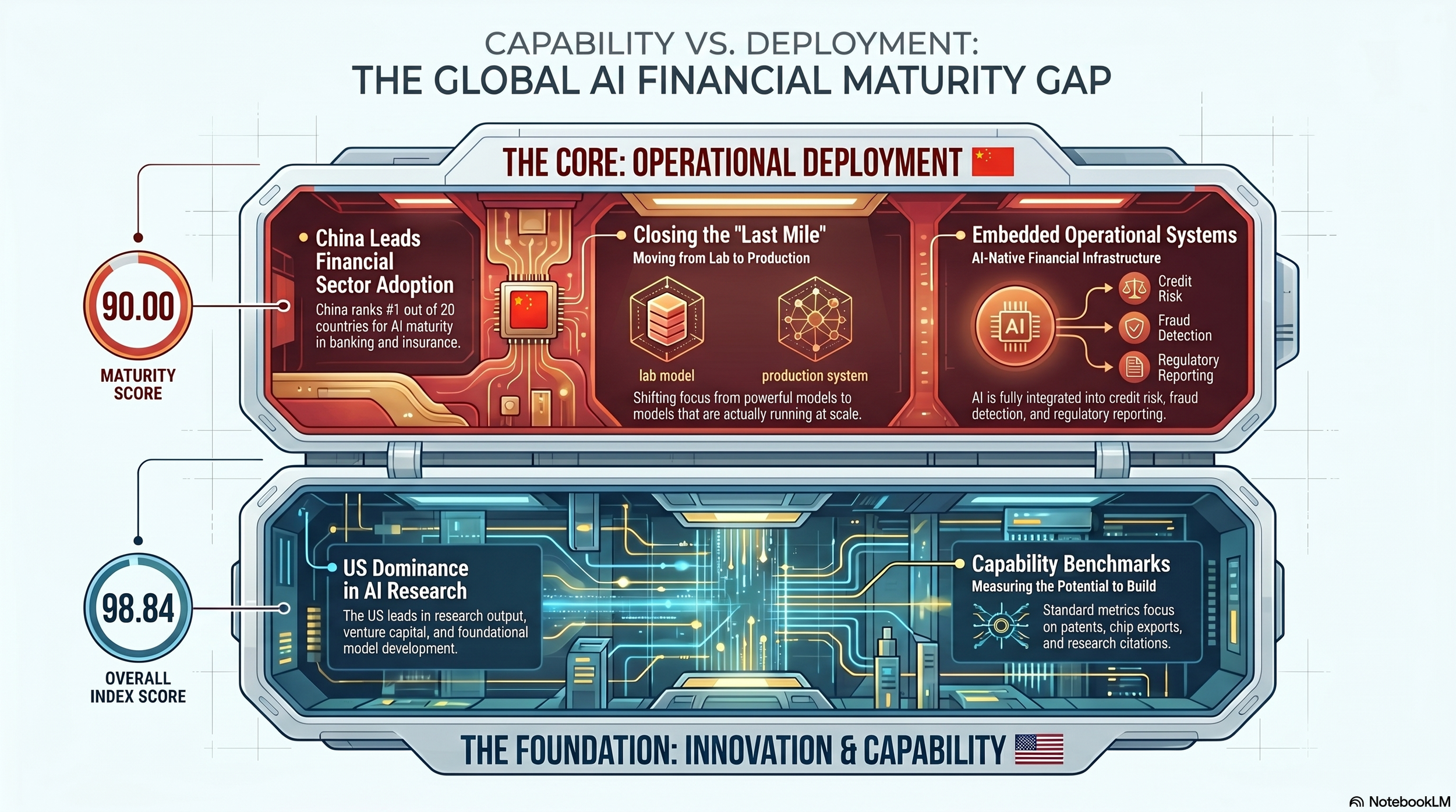

The United States leads the overall country index with a score of 98.84. China follows at 83.41. On those headline numbers, the conventional hierarchy holds. But the index scores countries across multiple pillars, and on the pillar that specifically measures financial-sector AI maturity, China does not rank second. It comes first, with a score of 90, the highest of all 20 countries assessed, for its adoption of AI across banking, insurance, fintech, and investment management. The report describes China as the strongest among the top-ranked nations at translating AI capacity into production-grade deployment in financial services, characterising it as the leader in closing what it calls the last mile from capability to operational systems.

What Financial Sector Maturity Actually Measures

The distinction matters because it separates two things that most AI assessments treat as the same: the ability to build AI systems and to run them at scale within regulated institutions. A country can lead in research output, venture capital formation, and foundational model development while its financial sector remains cautious, fragmented, or structurally slow to adopt. That appears to be, at least in part, the US dynamic.

China's financial sector has absorbed AI into its core operations with a speed and breadth that few Western commentators have closely tracked. Its major banks have deployed AI in credit risk modelling, fraud detection, customer operations, and regulatory reporting at a scale that reflects institutional commitment rather than experimentation. The country's fintech sector, anchored by Ant Group and WeBank among others, has been running AI-native financial infrastructure for long enough that production-grade deployment is the baseline, not the aspiration.

The report does not present this as a vulnerability in the US position so much as a clarification of what the US leads on and what it does not. American financial institutions have been more deliberate, some would say more cautious, in embedding AI into regulated workflows. The regulatory environment has been a factor, but so has institutional conservatism at the major banks, which have tended to pilot AI aggressively while scaling it carefully.

The Last Mile Is Where Competitive Advantage Accumulates

The report's framework treats the last mile from capability to deployment as the decisive competitive variable in AI-enabled finance. Capability without deployment generates research prestige and geopolitical leverage, but it does not produce the compounding operational advantages that come from AI systems running inside financial institutions at scale: the risk models that improve with every transaction, the compliance systems that adapt to new regulatory requirements in near real time, the fraud detection that tightens with every attempted breach.

China's score of 90 on financial sector AI maturity suggests it has been accumulating those advantages. Its combination of ecosystem scale and rapid implementation dynamics, as the report characterises it, reflects a financial system that has treated AI adoption as an operational priority rather than a strategic initiative.

What the Gap Means

The gap between leading in AI capability and leading in AI deployment in finance is not permanent, and the report does not suggest that the US is falling behind in any structural sense. American financial institutions are scaling AI adoption, and the country's overall index score of 98.84 reflects genuine multi-pillar depth. But the China finding should prompt a more specific question than the usual framing of US-China AI competition invites.

The standard comparison focuses on who is building the most advanced models, who is filing the most patents, who is attracting the most capital into AI research. Those are legitimate measures of capability. The GAICI Part 5 adds a measure that has been largely absent from the conversation: who is running the most AI, inside the most systemically important institutions, in the most operationally consequential ways.

On that measure, China leads. And as Dr Patrick Glauner, Professor of AI at Deggendorf Institute of Technology and a co-author of the report, noted in the report's release, deployment quality matters as much as innovation in finance. The models that matter most are not the most powerful ones. They are the ones that are actually running.