One in Eight Jobs, Transformed: The AI Automation Report That Should Worry the Boardroom

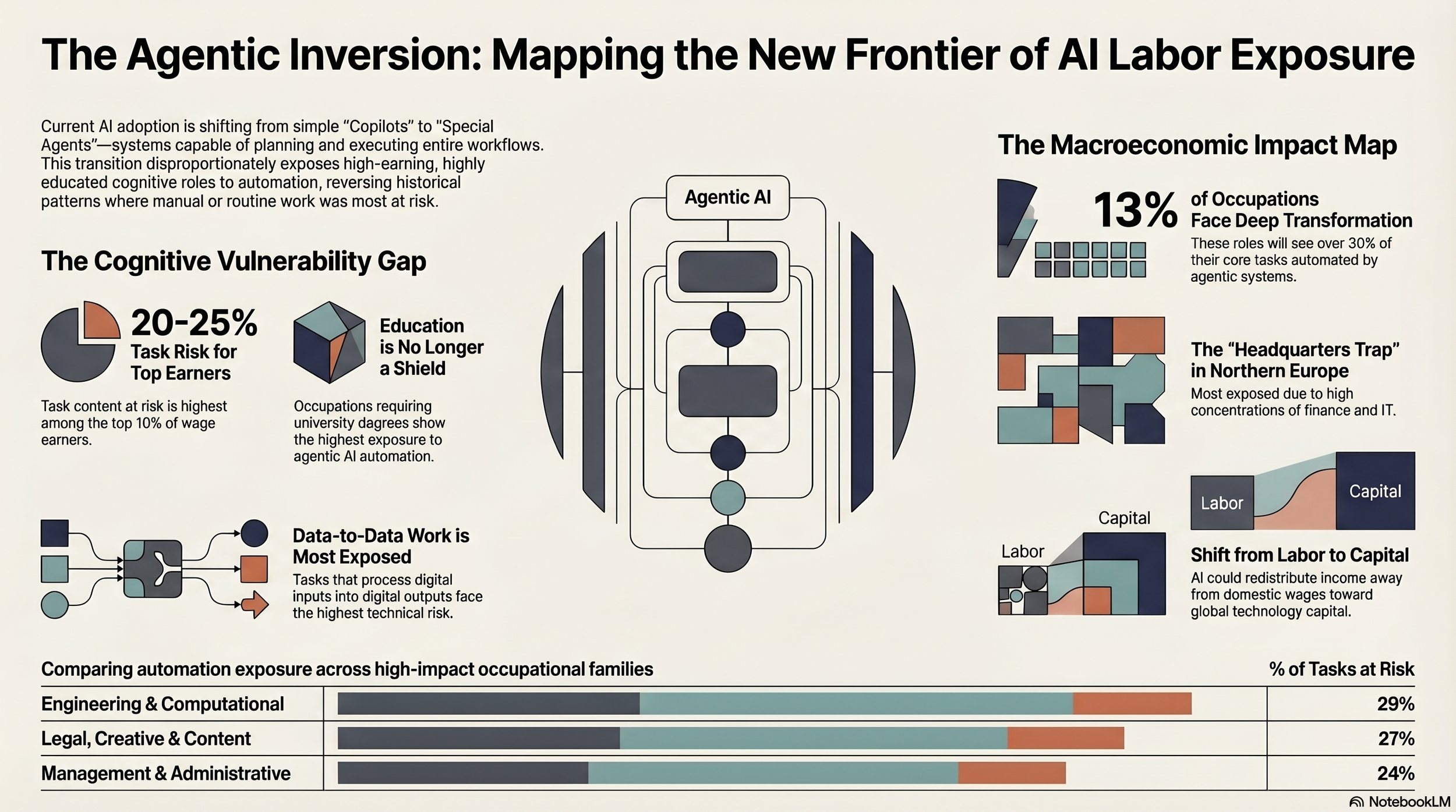

Consider a handful of numbers. One in eight occupations will have more than 30% of their tasks automatable by agentic AI in the coming years. Between 14% and 20% of all workforce tasks — depending on the country — could be automated. Among the highest-paid 10% of workers, 20 to 25% of their tasks are already in the crosshairs. And in engineering and computational roles, the single most exposed occupational family has a figure of 29%. These are not projections about robots on factory floors. They are projections about lawyers, analysts, engineers, and managers — the people who, until very recently, had every reason to feel secure.

Three years after ChatGPT arrived and upended corporate imagination, artificial intelligence remains conspicuously absent from the statistics that economists actually care about. Hiring figures, wage growth, and unemployment rates — none of them yet show the disruption that boardrooms have been bracing for. But a major new study warns that the absence of evidence is not evidence of absence. The share of companies reporting AI use in at least one business function rose from 55% to 88% between 2022 and 2025, while adoption of generative AI alone leapt from 33% to 79%. The effects that are visible so far are concentrated at the margins: weaker entry-level hiring in AI-exposed firms, quiet wage pressure on junior roles, and — in France and the United States alike — employment declines clustered among workers at the very start of their careers. What current studies may be capturing, the authors suggest, is “less the main shock than its early signal.”

The research, produced jointly by credit insurer Coface and the Observatoire des Emplois Menacés et Émergents (OEM), maps the automation exposure of 923 occupations across more than 30 countries along five successive phases of AI development. Its conclusion is striking: the occupations most vulnerable to the next wave of automation are not the ones that previous technological disruptions targeted. This time, the machine is coming for the knowledge worker. As the report puts it, “AI is not being deployed on the fringes of work, but across a section of its cognitive, non-routine and skilled functions — long perceived as the most secure.”

A Different Kind of Disruption

Earlier waves of automation followed a recognisable pattern. Industrial robotisation displaced manual labour in factories; rule-based software swept through routine office work in the 2000s. Both concentrated on the middle of the skills distribution, hollowing out routine, middle-skill jobs while leaving highly educated workers largely undisturbed — the phenomenon economists call labour market polarisation.

The current AI wave breaks this pattern. The report finds that “the automation potential of AI in its agentic form is highest in occupations made up largely of cognitive, non-routine tasks often performed by more highly educated and better-paid workers.” Engineering and computational occupations face the highest exposure, with 29% of task content at risk; legal and financial occupations at 27%; and management and administrative roles at 24%. By contrast, in-person manual services and skilled trades sit below the 10% threshold. “Where previous waves hollowed out the middle of the income distribution,” the study warns, “the current wave threatens to compress it from the top.” To arrive at these figures, the OEM decomposed each of the 923 occupations into tasks, then broke those tasks down further into elementary actions — each defined by a verb, a direct object, and a contextual element — and scored every action using explicit, reproducible semantic rules across five technological phases. The framework deliberately measures “technical exposure to automation, not net job destruction” and does not account for new tasks AI might create, or the organisational and regulatory frictions that slow deployment in practice.

One in Eight Jobs Facing Deep Transformation

Under the study’s central scenario — the emergence of agentic AI, where multiple models are orchestrated together with access to tools such as search, file systems and email — 120 of the 923 occupations studied cross a 30% automation threshold, which the researchers identify as a marker of profound structural transformation. Among them, 56 belong to high-skill families, including computer and mathematical, architecture and engineering, and legal occupations. “Expertise and formal knowledge alone,” the study concludes, “no longer shield an occupation.”

The most protected roles are those anchored in physical dexterity and real-time sensory feedback. Metal pourers and painting workers have exposure below 0.3%. Mental health counsellors score 8.2%, child and family social workers 9.1% — protected not by the depth of their knowledge but by what the study calls “continuous adaptation to contextually unique human situations: relational attunement and improvised judgement that cannot be reduced to pattern-matching over historical data.”

Automation-exposed task content ranges from around 12% in Turkey to nearly 20% in the United Kingdom, with France at 16%, Germany at 17%, and the United States at 17%. The wealthiest, most cognitively oriented economies are the most exposed. Luxembourg tops the European table at 21%, followed by Ireland and Switzerland — all reflecting high concentrations of finance, IT and legal employment. GDP per capita, the study finds, is “the most useful single heuristic for approximating AI exposure across countries.”

For the Gulf region, the stakes are particularly pointed. The sectors most exposed to agentic AI — finance, legal services, management consultancy, information technology — are precisely those that the UAE and Saudi Arabia have spent the better part of a decade building as the pillars of economic diversification. Yet Mohamad Jomaa, CEO and Country Manager for GCC and Egypt at Coface, sees the moment not as a threat but as a defining strategic opportunity. “The UAE and Saudi Arabia are moving decisively to position themselves as global AI and compute hubs,” he says. “Commitments measured in the tens of billions of dollars — including multi-gigawatt data centre campuses, advanced GPU capacity, and national AI platforms — signal a clear understanding that AI competitiveness starts with infrastructure. These are not pilot initiatives; they are long-term, sovereign-level investments designed to anchor economic diversification and global relevance in a data-driven world.” For Jomaa, the nations that move earliest to own the infrastructure of the AI economy are best placed to capture its productivity gains, rather than simply absorb its disruptions.

The Macroeconomic Stakes

The implications extend well beyond job counts. The study warns of “a significant redistribution of income away from labour and toward capital.” If losses in exposed occupations are not offset by new job creation, productivity gains will accrue first to companies deploying AI, then further upstream to technology companies controlling the AI value chain. For governments that rely heavily on taxing labour, this creates a double fiscal challenge: reduced revenue at precisely the moment public expenditure on unemployment support and retraining rises. The study flags “a double risk of erosion of the domestic wage tax base and partial leakage of capital income toward foreign countries where AI profits are concentrated.”

Education faces its own reckoning. Data across Canada, Sweden, Germany, the Netherlands and Japan show a clear correlation: the more educated a worker, the greater their exposure to agentic AI. Figures including Sam Altman and Jensen Huang have questioned whether degrees will retain their labour-market value, while academics like Erik Brynjolfsson and Daron Acemoglu argue higher education must adapt towards judgement, supervision and analytical literacy rather than knowledge transmission alone. The study does not adjudicate between these views, but frames the underlying challenge clearly: if some of the tasks for which long courses of study prepare workers become more easily automatable, “the link between educational attainment, pay and job security could weaken.”

There is also a geopolitical dimension. By shifting production toward more concentrated forms of capital, an AI-intensive economy increases exposure to systemic vulnerabilities — export controls, semiconductor supply constraints, cloud service disruptions. The key assets underpinning AI remain “highly concentrated across a small number of companies and countries,” the study warns, “thereby increasing exposure to external shocks, regulatory frictions and strategic vulnerabilities.” Even as AI raises productivity broadly, it may simultaneously create new single points of failure through which shocks propagate.

The researchers are careful to note that the framework is not a forecast. The translation from gross technical exposure to actual employment effects “is neither immediate nor mechanical.” It abstracts away from demand dynamics, the potential creation of new roles, and the organisational inertia that will slow adoption in many workplaces. But the underlying questions, the authors insist, would remain even under a more gradual scenario. The occupations being targeted are not peripheral to modern economies — they are central to income formation, tax revenues and value creation. A transformation of this scope, however gradually it unfolds, seems unlikely to leave the structure of work, wages or welfare states unchanged.

“The framework should be understood,” they write, “not as a forecast, but as a structured map of where labour-market, macroeconomic and strategic pressures are most likely to emerge as agentic AI diffuses.” The automation frontier has moved. It now runs through the cognitive heart of the modern workforce — and the early signals, for those paying attention, are already here.