Closing the Venture Capital Gap for Female Founders Would Add $5 Trillion to Global GDP. In 2026, That Gap Is Getting Wider.

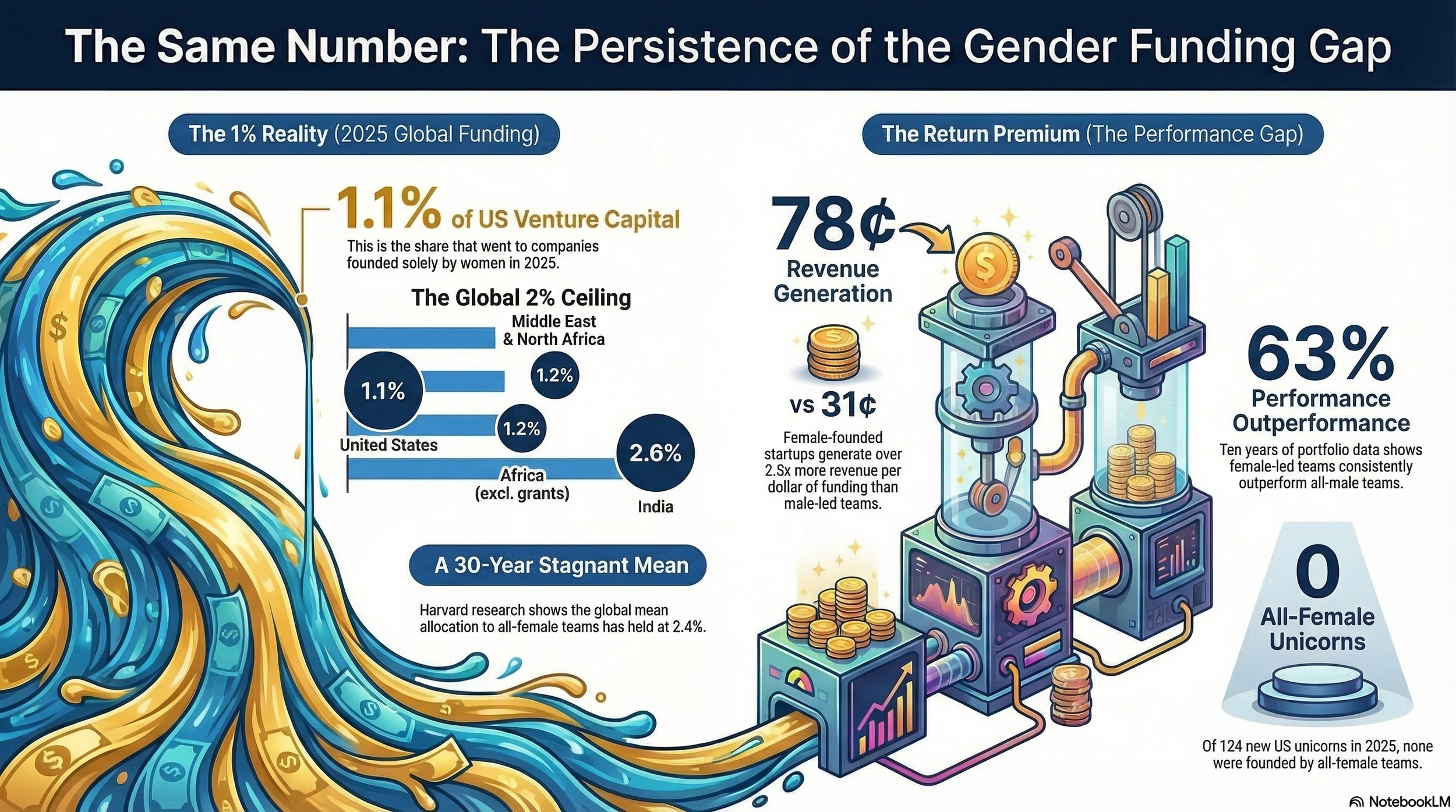

1.1%. That is the share of US venture capital that went to companies founded solely by women in 2025. Across the Atlantic, in Europe, all-female founding teams in 2025 were on track to raise less than one billion euros for the year, the first time since 2020. In Africa, women-led startups raised just 2% of total venture funding, and less than 1% if grants are excluded. In the Middle East and North Africa, the figure was 1.2%. In India, with one of the world's fastest-growing startup ecosystems, women-only founding teams received 2.6% of total venture capital. The numbers change as you move around the map. The story does not.

This piece is not about why that is unfair. It is about why, in 2026, with twenty years of performance data, a documented and replicated return premium, thousands of published reports, and a growing ecosystem of funds built explicitly on the thesis that this gap represents a mispricing, the number has not moved in any meaningful direction on any continent. That is not a social question. In any other asset class, it would be called a market failure.

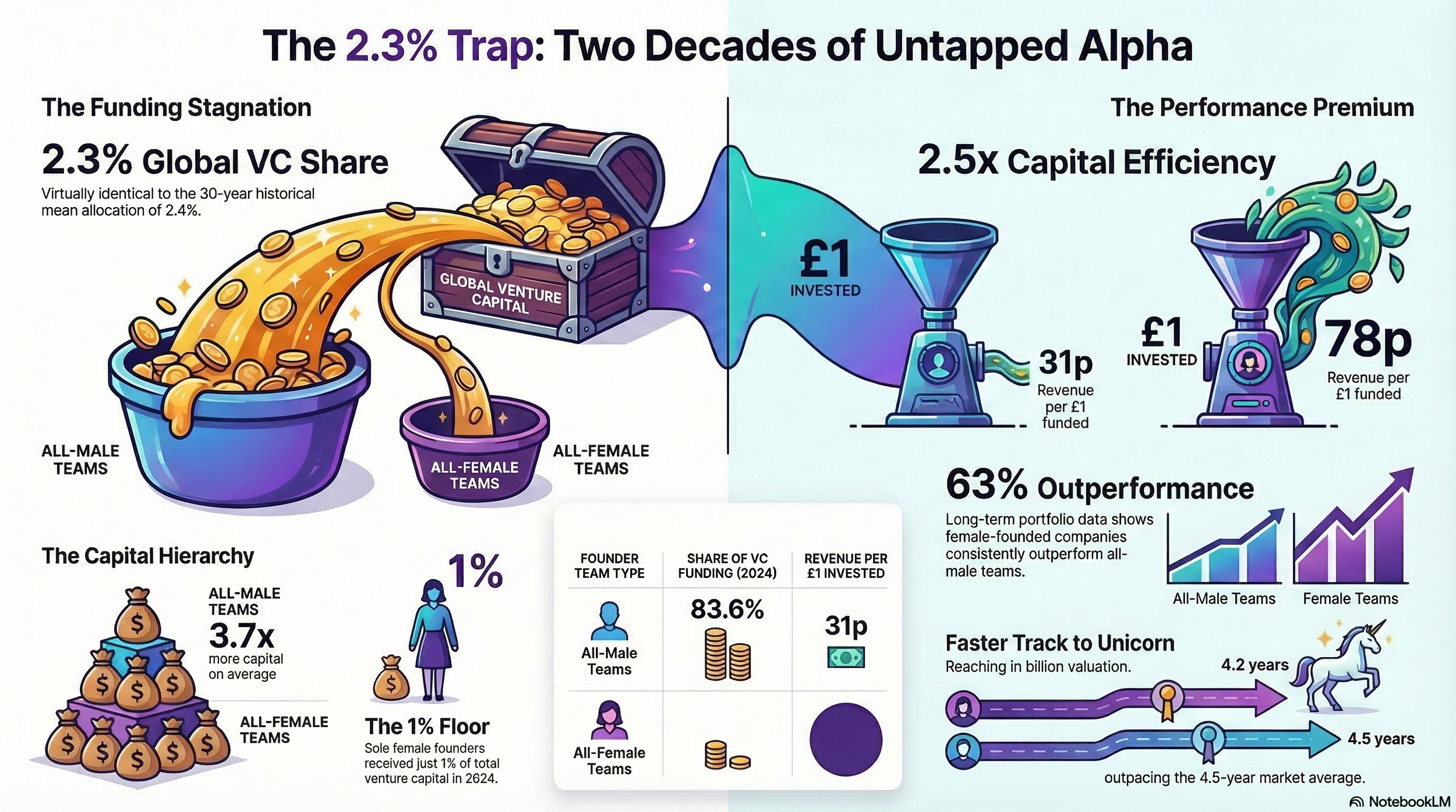

The pattern is consistent enough that Harvard's research programme on venture capital and entrepreneurship has tracked the long global average: over thirty years, the mean allocation to all-female founding teams has held around 2.4%. The current figures, in almost every market on earth, are at or below that mean. The conversation about closing the gap has, in large part, been about mixed-gender teams. The sole female founder, building alone, raising alone, sits at the very bottom of a capital hierarchy that has remained structurally unchanged for two decades and, in 2025, moved further in the wrong direction.

The Data – Flat

The 2025 picture from PitchBook's annual All In: Female Founders in the VC Ecosystem report, published in March 2026, requires two readings. The first is the US headline: female-founded companies raised a record $73.6 billion, capturing an unprecedented 27.7% of total US venture deal value. The second is what sits beneath it. More than $30 billion of that figure came from just two companies, Anthropic, co-founded by Daniela Amodei, and Scale AI, co-founded by Lucy Guo.

Together, they account for over 40% of all AI funding going to female-founded companies. Strip those two names from the data, and the record not only shrinks but falls below the prior year. Meanwhile, companies founded solely by women in the US raised just 1.1% of venture capital dollars in 2025, down from 2.1% in 2024. All-female teams raised a combined $3.2 billion across 794 deals. All-male teams raised $191.1 billion across 10,048 deals. While all-male founding teams raised 21% more capital than the year before, all-female founding teams raised 22% less.

In Europe, PitchBook's companion 2025 European All In report tells the same story with different numbers. Female-founded companies collectively raised 9.5 billion euros across more than 1,800 deals in 2025, marking a steeper decline from 2024 than the European market as a whole. Their share of overall dealmaking slipped to just 16.5% of deal value, down from 20.4% the year before. For all-female founding teams specifically, deal value and count both fell, and at the current trajectory, they were unlikely to break the one billion euro mark, a threshold last missed in 2020. In AI, Europe's most active and generously funded sector in 2025, female founders captured only 3 billion euros of the 23.5 billion euros deployed, despite the sector being the primary driver of capital across the continent.

Across emerging markets, the picture worsens. In Africa, more than $2 billion was raised by startups in 2025, with roughly 10% going to companies that included at least one female founder. Women-only founding teams received a fraction of even that. In sub-Saharan Africa, female-led startups raised $48 million in 2024, compared with $2.2 billion for male-led startups, a gap that is not a percentage problem but a structural one: even when women break into competitive sectors, support skews toward grants rather than equity, leaving most unable to scale on their own terms.

In India, women-only teams saw 2.6% of a $12.5 billion startup market. In Latin America, Colombia directed 5.7% to women-only teams and Mexico 4.5%, while Brazil lagged at 3.3%.

The hierarchy is consistent across every geography. All-male founding teams raise, on average, 3.7 times more than female-only teams globally. Adding a male co-founder more than doubles a founder's access to capital in every major market studied. The gap is not between men and women.

It is between men, mixed teams, and women building alone, and it compounds at every stage of the funding journey. By the late stage, the average female-founded company carries a valuation discount relative to the market average that it did not create and cannot individually resolve. The median Series A pre-money valuation gap between all-female founding teams and the broader US market widened fivefold between 2014 and 2025.

The Rewind

The 2025 headline is technically accurate in the US. The sole female founder's share went down everywhere. Both things are true simultaneously, which is precisely the structural point the timeline makes. Capital is concentrating, not distributing. Two companies lifted the US headline. The rest of the global market moved in the other direction.

The timeline starts in 2005 in the venture data. That year, women-founded companies accounted for 7% of first VC financings in the United States. In the same period, in Europe, Africa, and Asia, the conversation was barely being had. By 2015, First Round Capital, one of the most respected seed funds in the US, published ten years of portfolio performance data.

Female-founded companies in its portfolio had outperformed all-male founding teams by 63%. The report was widely covered across every market. The number held in every market.

By 2017, first financings for women-founded companies had reached 21% in the US, a genuine gain at the entry gate. The dollars did not follow. In 2021, the largest venture capital market in recorded history deployed $330 billion globally. Women received their lowest percentage share in five years. The 30-year Harvard average for all-female founding teams is 2.4%. The 2025 figure for sole female founders is 1.1% in the US, and lower still across most of the rest of the world. In statistical terms, there is no trend toward improvement. There is a trend in the other direction.

A small number of investors identified the mispricing early. Golden Seeds has operated as an angel and early-stage investment network since 2004, built on the explicit thesis that gender-diverse teams produce better return on equity.

Since its founding, its members and funds have invested over $180 million in 249 companies, which have since raised over $2 billion in additional capital. That follow-on multiplier is the core metric of early-stage fund quality. The arbitrage was identifiable in 2004. It remains identifiable and worsening across every major market in 2025. The broader global capital system has not moved to capture it.

The Return Premium Nobody is Collecting

In 2018, the Boston Consulting Group published a study of 350 companies that had passed through the MassChallenge accelerator programme, controlling for sector, educational background, and pitch quality. For every dollar of funding, female-founded startups generated 78 cents in revenue. Male-founded startups generated 31 cents. That is not a marginal difference. It is a 2.5-times gap in capital efficiency, replicated across independent datasets in multiple markets and sustained over time.

The finding does not stand alone. First Round Capital's decade of portfolio data shows female-founded companies outperformed all-male teams by 63%. The Kauffman Fellows Report puts women-led teams at a 35% higher return on investment. Illuminate Ventures found that women-led companies in the early stages reached revenues comparable to those of male-led counterparts while using, on average, one-third less capital.

PitchBook's 2025 data shows female founders' share of US exit count reached nearly 25%, a record high, despite holding 1.1% of deployed capital. In Europe, more than two-thirds of female-founded startups raised a follow-on round or exited after their initial VC financing in 2025, slightly outperforming the total European figure, while female-founded unicorns reached a record-high aggregate valuation across the continent.

In 2025, the United States produced 124 new unicorns. Twenty had at least one female founder. Not one was founded by an all-female team. In the first half of 2025, every new unicorn in Europe and the United Kingdom had a solely male founding team.

Serena Ventures, founded in 2014 on the thesis that underfunded founders are underpriced founders, has produced 16 unicorns across 85+ portfolio companies, with a total portfolio valuation of $33 billion. The performance case has been made, demonstrated, and repeated. Female-founded companies perform well and exit well across every major market studied. They are not funded in proportion to either.

In any other asset class, a consistent, independently replicated return premium of this magnitude, documented across BCG, First Round, Kauffman, Illuminate, and PitchBook, and observed across the US, Europe, and emerging markets, would trigger reallocation. In venture capital, in every geography, it has triggered reports.

Capital is not Neutral

Heather Henyon is the Founding Partner of Mindshift Capital, a global venture firm investing in women-led early-stage technology companies across the United States, Europe, and the Middle East. She has spent over twenty years in international finance, with fifteen of those based in the Gulf. The geographic breadth of her work gives her a specific vantage point on why the gap persists across markets that are otherwise very different from each other. When she talks about how capital costs founders more than the check itself, she is not speaking abstractly.

"The money itself is not just money anymore," she said. "The source of capital can shape later choices around expansion, follow-on funding, strategic partnerships, acquisitions, and eventual exits. If you choose a structure that is easy in the short term but becomes hard to work with later, you may be giving up future flexibility without realising it."

That observation applies with equal precision across every geography. In the US, a smaller first check compounds into a lower Series A valuation and a weaker growth-stage position. In Europe, all-female founding teams are heading toward a year in which they may not break the one billion euro mark for the first time in five years, not because they stopped building but because the structural conditions for accessing later-stage capital have not been built around them.

Henyon is direct about what this means for founders navigating regulated industries, several of which Mindshift backs. "Regulatory risk is real and can shape the economics of the business just as much as customer demand does," she said. One of Mindshift's portfolio companies, Vivoo, a Turkish-founded healthtech business earning most of its revenue from the US market, made a deliberate early decision to position itself in the wellness space rather than as a medical device. The distinction is not cosmetic.

"That decision affected the entire company journey," Henyon said. "It shaped speed, cost, go-to-market, and the kinds of risks they had to manage."

This matters for female founders disproportionately because the sectors where women are most concentrated globally, healthtech, femtech, edtech, consumer wellness, carry the highest regulatory burden and attract the lowest valuation multiples in every market. Femtech alone addresses a global market projected to exceed $103 billion by 2030, yet receives 1.4% of total investment.

Women are building in lower-ceiling markets not by accident but because those are the markets where they have identified unsolved problems. The lower ceiling then becomes evidence, in investors' pattern-matching, of lower ambition.

The geographic compounding is acute. Henyon observes that for founders across MENA, Africa, Turkey, India, and Southeast Asia, access to US or European capital is both strategically rational and structurally costly.

"As companies move into later-stage fundraising, there is often less available capital in the region, and it can be harder to access the kinds of rounds they need to keep scaling," she says. The IFC estimates just 7% of total private equity and venture funding in emerging markets targets women-led businesses. Africa forfeits an estimated $95 billion in economic potential annually due to gender inequality, according to the United Nations Development Programme. In a region where 47% of STEM graduates are women but only 23% enter the tech workforce, and even fewer enter tech leadership, the funding gap is not an isolated financial statistic. It is a compound economic problem.

Henyon is precise about what alignment with external capital actually means in practice. "The problem is not foreign capital. The problem is misaligned capital," she says. "If the investor base reflects one geography but the business reality reflects another, tensions can emerge later. Investors often influence expansion priorities, hiring, governance expectations, and exit paths." A female founder in Lagos or Riyadh or Mumbai who accepts capital from an investor whose network, assumptions, and exit thesis do not match her operating reality has not just accepted money. She has accepted a set of constraints that will shape every decision that follows.

The answer, in Henyon's view, requires structural discipline before anything else. "Temporary solutions often turn into permanent problems," she says. "A lot of entrepreneurs focus on cost in the early days, and I understand why. They want to preserve runway, so they pick a free zone setup, or an inexpensive local structure, or something that feels good enough for now. But then, once they raise institutional capital, or want to expand, or need to move assets and IP, it becomes painful."

For the sole female founder starting with less capital and less runway than her male counterparts, in any market on earth, that window for structural error is narrower from the start.

What the number costs

The McKinsey Global Institute estimates that if women participated in the economy at the same rate as men, the addition to annual global GDP would approach $28 trillion. The more focused estimate, specific to closing the venture capital funding gap, is $5 trillion. That is not a projection of equality. It is a calculation of foregone economic output, what the current mispricing is costing the global market, every year it continues, across every geography where it persists.

The funds that have operated on the return thesis, Golden Seeds since 2004, Female Founders Fund since 2014, Mindshift Capital since 2018, Serena Ventures building toward 16 unicorns, are not exceptions to the rule. They are proof that the arbitrage is real and capturable in multiple markets simultaneously. In 2025, 127 women-led venture capital funds closed on a combined $2.45 billion globally. The capital base dedicated to this thesis is growing. The broader market, in every region, has read the same data and has not followed.

The 2025 numbers are the starkest version of the story the data has been telling for two decades. A record headline figure in the US, driven by two AI companies. A falling share in Europe. A 2% ceiling in Africa that drops below 1% without grants. A narrowing pipeline in every market, with the share of female founders receiving their first venture check falling from 27.7% in 2021 to 21.2% in the US by 2025. The pattern is global, consistent, and worsening in 2025. And 82% of decision-makers at major VC firms worldwide remain male, the figure that sits upstream of all the others.

Henyon's final observation is the one that settles the argument. Asked to distil this moment into a single lesson for founders operating across these conditions, she does not reach for encouragement. She reaches for architecture.

"Treat structure as strategy, not paperwork," she said. "Where you incorporate, where your IP sits, where your investors come from, which market you enter first, and how exposed you are to one jurisdiction. These are no longer backend decisions. They shape optionality, speed, resilience, and even survival. Founders still have to build a product people want. That part has not changed. But increasingly, they also have to build a company that can survive the political and regulatory world it lives in. And that requires thinking much earlier, and much more carefully, about the architecture around the business, not just the business itself."

That advice is directed at any founder navigating a complex capital environment. For the sole female founder in 2026, whether she is building in San Francisco, London, Nairobi, Dubai, or Mumbai, the environment has been structurally hostile for twenty years, not through malice but by design. The market has been built in a particular shape, and that shape produces the same output across radically different geographies. The consequences are measurable. They have been measured, repeatedly, by multiple independent institutions, on every inhabited continent.

In 2026, with that full body of evidence available, the sole female founder's share of venture capital is 1.1% in the US, below 1% in Africa without grants, 1.2% in MENA, and declining in Europe. It was around those figures, give or take a decimal, when the first reports were written two decades ago.

In financial terms, a mispricing that has been identified, documented, replicated across independent studies, demonstrated in fund returns over twenty years, and observed across every major venture market on earth, without correction, is no longer a market inefficiency waiting to be arbitraged. It is a feature of the market's current design. The question is not when these changes.

As Henyon puts it: "It is no longer just about who will fund you. It is about what kind of future that funding enables or quietly restricts." For the sole female founder in 2026, that question has the same answer it had in 2005, in every language, in every market, on every continent where the data has been collected.